Headline Measures

From 1 July 2027, the ability to claim rental property losses against wages and other income will be restricted to new residential builds only. Investors who buy established properties after Budget night will only be able to offset losses against residential property income — not wages. Properties owned at Budget night are fully protected and not affected.

The 50% CGT discount — in place since 1999 — will be replaced from 1 July 2027 with inflation-based cost indexation and a minimum 30% tax on gains. This affects all individuals, trusts and partnerships selling shares, investment properties and other capital assets. Assets already owned get transitional protection — only growth after 1 July 2027 falls under the new rules. Pre-1985 assets (previously CGT-free forever) are also brought into scope for the first time.

From 1 July 2028, a minimum 30% tax will apply to all income distributed from discretionary (family) trusts — paid at the trustee level. This effectively ends decades of income-splitting flexibility. Beneficiaries receive a non-refundable credit for the trustee's tax, but low-rate beneficiaries no longer produce a real tax saving. Bucket companies lose the strategy entirely. Fixed trusts, superannuation funds, deceased estates and charitable trusts are excluded.

Businesses

Small businesses with annual turnover under $10 million can now permanently write off individual assets costing under $20,000 in the year of purchase. Previously renewed year-by-year, this has been made permanent from 1 July 2026, giving businesses long-term certainty when planning equipment purchases.

From 2026–27, companies with turnover up to $1 billion that make a loss can apply that loss against tax paid in the prior two income years, receiving a cash refund from the ATO. Additionally, from 2028–29, small start-ups in their first two years of operation can receive a refund for losses up to the value of FBT and wage withholding tax already paid.

The full FBT exemption for electric cars under $75,000 continues for arrangements entered into before 1 April 2029. From 1 April 2029, this becomes a permanent 25% FBT discount. New from 1 April 2027: electric cars between $75,000 and the luxury car tax threshold gain a 25% discount for the first time. Existing arrangements are grandfathered.

From 1 July 2027, businesses can opt into monthly PAYG instalments rather than the standard quarterly cycle. The ATO is also expanding its dynamic instalments tool, which uses accounting software to calculate more accurate instalments based on actual business performance.

Individuals

A new permanent $250 tax offset for every working Australian, automatically applied to tax returns from the 2027–28 income year (first received in the July 2028 tax return). It applies to wages, salaries and sole trader business income, and effectively raises the tax-free threshold slightly to just under $20,000.

From the 2026–27 tax year — this year's return — workers can claim up to $1,000 in work-related expense deductions without needing to keep receipts. Around 6.2 million Australians benefit, saving an average of $205. Those claiming more than $1,000 still need receipts for the full amount. Other deductions such as donations are still claimable on top.

Currently, Australians aged 65 and over receive a higher government rebate on private health insurance premiums. From 1 April 2027, this age-based uplift is removed — older Australians move to the standard rebate rate, meaning their net out-of-pocket premium will increase. The income testing of the base rebate is unchanged.

Previously Announced / Already Underway

These cuts are law — no uncertainty. The rate on income between $18,201 and $45,000 has already dropped from 19% to 16% (from 1 July 2024), drops again to 15% from 1 July 2026, and falls to 14% from 1 July 2027. For anyone earning above $45,000, this means an extra $268 per year in 2026–27 and $536 per year from 2027–28 compared to pre-2024 rates. Changes flow through automatically via payroll.

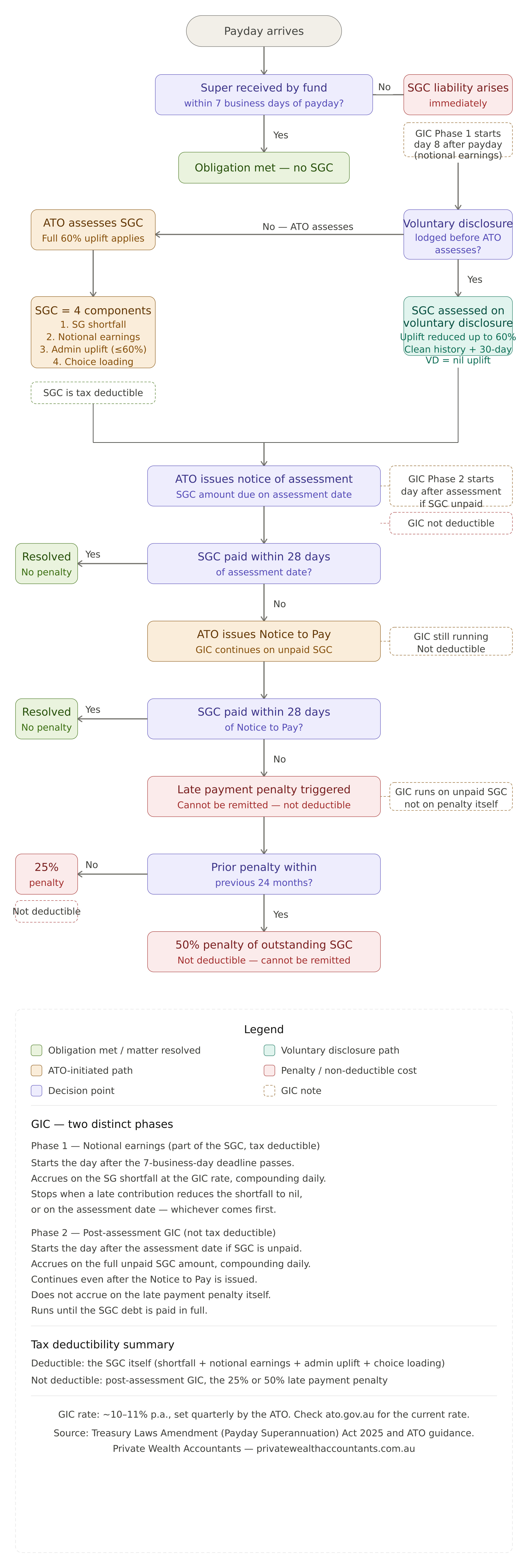

From 1 July 2026, employers must pay superannuation at the same time as wages — replacing the old quarterly payment cycle. This was legislated before the Budget. For employees, it means faster compounding in super and better protection if an employer runs into financial difficulty. For employers, payroll systems must support more frequent super payments.

Negative Gearing — Full Analysis

Announced 12 May 2026 · Proposed start: 1 July 2027 · Not yet law

Negative gearing is one of the most widely used tax strategies in Australia. The proposed changes are significant — but whether you are affected depends entirely on when you bought or plan to buy your investment property.

What is Negative Gearing?

Negative gearing occurs when a rental property costs more to own and operate than it earns in rent. The gap — the rental loss — can currently be deducted against any other income, including wages. This reduces your taxable income and therefore the tax you pay.

Sarah earns $120,000 in wages. Her investment property generates $26,000 in rent but costs $38,000 to hold — interest, rates, insurance, repairs and depreciation. Her rental loss is $12,000.

Under current rules: that $12,000 reduces her taxable income to $108,000 — saving roughly $3,900 in tax at her marginal rate. The tax office effectively subsidises part of the cost of holding the property.

How the Changes Apply — By When You Bought

From 1 July 2027: losses can only offset residential property rental income or capital gains from property sales — not wages or other income. Unused losses carry forward indefinitely to future years.

What Counts as a "New Build"?

Not every recently constructed property qualifies. To retain full negative gearing, the property must genuinely add new housing to supply:

- A newly constructed dwelling on vacant land

- A knock-down rebuild that creates more dwellings than before

- An off-the-plan apartment or house-and-land package

- Build-to-rent developments and properties supporting government housing programs

- A resale of a property that was originally a new build — second and subsequent purchasers do not retain new-build status

- A renovation that does not increase the number of dwellings

- Commercial property — not affected by these changes at all; existing rules continue

What is Completely Unaffected

- Shares and other investments: Negative gearing on a share portfolio is entirely unchanged.

- Commercial property: Losses remain deductible against all income — no change.

- SMSFs and widely held trusts (e.g. managed funds): Excluded from the changes.

- Build-to-rent and government housing programs: Specifically carved out.

When You Eventually Sell — Carried-Forward Losses

For investors who buy established property after Budget night, unused rental losses carried forward don't disappear on sale. They can be applied against the capital gain on sale, reducing the CGT payable. So while the immediate annual tax saving is deferred or eliminated, it can still be partially recovered on exit.

Who is Most Affected?

- High-income earners buying established investment properties after Budget night — the immediate tax benefit is gone

- Investors relying on the annual tax saving to help service loan repayments

- Those buying in the transitional window expecting to claim losses against wages indefinitely

- Anyone who owned property (or was under contract) at Budget night — fully grandfathered

- New build investors — full deductibility retained

- SMSF investors — excluded from changes

- Share and managed fund investors — no change

Capital Gains Tax Changes — Full Analysis

Announced 12 May 2026 · Proposed start: 1 July 2027 · Not yet law

The CGT changes are the broadest tax reform in this budget. They affect almost every type of investment asset held by individuals — not just property — and introduce new complexity for anyone planning to sell assets in future years.

The Current System (Before 1 July 2027)

When you sell an asset for a profit, you pay Capital Gains Tax. The defining feature of the current system — introduced in 1999 — is the 50% discount: if you've held the asset for more than 12 months, only half the gain is included in your taxable income. There is no minimum tax rate — if your income is low in the year you sell, you pay at a low marginal rate.

James bought an investment property for $500,000 in 2015 and sells in 2026 for $1,100,000 — a $600,000 gain. The 50% discount applies. He includes only $300,000 in his taxable income. At a 37% marginal rate, he pays roughly $111,000 in tax — an effective rate of about 18.5% on his actual gain.

If James happened to be in a low-income year when he sold (e.g. just retired), he could pay an even lower rate on that discounted gain.

What Changes from 1 July 2027

For gains accruing from 1 July 2027, the 50% discount is replaced with two new elements:

- Cost base indexation: Your original purchase price is adjusted upward for inflation using CPI. You only pay tax on the "real" gain above inflation — similar to how CGT worked between 1985 and 1999.

- 30% minimum tax: After indexation, any remaining real gain is taxed at a minimum of 30%, regardless of your income level. This prevents the strategy of timing asset sales to coincide with a low-income year.

Which Assets Are Affected?

- Shares, ETFs, managed funds and other investments

- Established residential investment properties

- Business assets held by individuals, trusts and partnerships

- Pre-1985 assets (see below)

- Cryptocurrency and other capital assets

- Your main home — the principal residence exemption is fully retained

- New residential builds — investors can choose between the old 50% discount and the new system at time of sale

- Superannuation funds — CGT rules unchanged

- Age pensioners and income support recipients — exempt from the 30% minimum tax

- Small business CGT concessions — the four concessions remain fully available for eligible small business asset sales

Assets You Already Own — The Split Treatment

If you own assets now and sell after 1 July 2027, a split approach protects gains already accrued:

The longer you've already held an asset, the greater the portion of your total gain that is protected by the 50% discount — only future growth falls under the new regime.

Establishing Your Asset's Value at 1 July 2027

The split treatment requires you to determine what your asset was worth on 1 July 2027. Two methods are proposed:

Obtain a professional valuation at 1 July 2027, or use a quoted market price (e.g. the closing share price on that date). This gives a precise figure reflecting actual market conditions.

Best for: assets where growth has been uneven — for example, a property that surged between 2020 and 2024 but has been flat since, or an asset that has recently declined. A proper valuation pushes more of the total gain into the pre-2027 discounted period.

The ATO will publish a formula estimating the 1 July 2027 value based on the asset's average annual growth rate over its full holding period. Simple and low-cost — no valuation required.

Best for: assets with steady, linear growth. Not ideal for: assets where growth has been heavily weighted to recent years — the formula will understate the 1 July 2027 value, attributing more of the gain to the post-2027 period and losing the 50% discount on it.

Pre-CGT Assets — A Significant Change

Assets acquired before 20 September 1985 have been completely exempt from CGT since the tax was introduced. This Budget proposes to end that permanent exemption for gains arising after 1 July 2027.

- Sold before 1 July 2027: Full exemption still applies — no tax, same as always.

- Still held on 1 July 2027: Gains accrued up to that date remain completely tax-free. The market value at 1 July 2027 becomes the new cost base, and only growth from that date forward will be taxed under the new indexation and minimum tax rules.

New Residential Builds — You Get a Choice

Investors in new residential builds can elect at the time of sale whether to apply the old 50% discount or the new indexation and minimum tax method — whichever is better. In practice, the 50% discount is generally better when the asset has grown strongly and inflation has been modest. Indexation is better when inflation is high relative to the asset's growth. This choice is not available for established property.

Who is Most Affected?

- High-income earners — effective CGT rate on post-2027 gains rises from ~23.5% to 30%

- People who planned to sell assets in a low-income retirement year to minimise CGT — the 30% minimum eliminates this strategy

- Investors holding assets through discretionary trusts — income-splitting of capital gains is curtailed

- Holders of pre-CGT assets expecting permanent exemption

- Your main home — principal residence exemption unchanged

- Super funds — CGT rules unchanged

- Age pensioners and income support recipients — exempt from minimum tax

- New build investors — can choose old or new method at sale

- Small business owners selling eligible assets — CGT concessions unchanged

Tax on Trust Distributions — Full Analysis

Announced 12 May 2026 · Proposed start: 1 July 2028 · Not yet law

Of the three headline measures, the trust changes are the most structurally significant — and potentially the most disruptive for family businesses and high-income investors. For the first time, a minimum tax will be imposed at the trust level, fundamentally altering the way distributions are taxed.

What is a Discretionary (Family) Trust?

A discretionary trust — also called a family trust — is a legal structure in which a trustee holds assets or runs a business for the benefit of a group of beneficiaries, typically family members. The defining feature is that the trustee has full discretion each year over who receives income and how much. This has historically allowed income to be directed toward family members on lower tax rates, reducing the overall tax burden for the family group.

For example: a family business operates through a trust. In a good year, the trustee distributes $80,000 to an adult daughter who is a full-time student with little other income. She pays a low rate of tax on it. This is income splitting — entirely legal under current rules, but exactly what the new minimum tax is designed to curtail.

The New 30% Minimum Tax — How It Works

From 1 July 2028, the trustee must pay a 30% minimum tax on the total taxable income distributed to beneficiaries. This is paid at the trust level first, as a separate obligation. Beneficiaries still include their share in their own tax return and calculate tax at their marginal rate, but non-corporate beneficiaries receive a non-refundable credit for the tax the trustee has already paid. Corporate beneficiaries receive no credit at all.

Scenario A — Beneficiary already on 30%+ tax rate: A trust distributes $100,000 to a beneficiary earning $130,000 in wages. Trustee pays $30,000 minimum tax. The beneficiary's own tax on the $100,000 is around $37,000. The $30,000 credit reduces this to $7,000. Total tax: $37,000 — same as before. No extra tax.

Scenario B — Beneficiary on a low tax rate (e.g. adult student): A trust distributes $40,000 to an adult child with no other income. Under old rules: around $3,200 in tax. Under new rules: trustee pays $12,000 (30% × $40,000). The student's own liability is only $3,200 — the credit reduces it to zero, but the remaining $8,800 credit is non-refundable and is lost. Net tax: $12,000 — nearly four times what it was. Income splitting to low-rate beneficiaries no longer works.

The "Bucket Company" Problem

A common strategy involves distributing trust income to a company — a "bucket company" — taxed at the 25% or 30% company rate, parking profits there and distributing dividends when convenient. Under the new rules, corporate beneficiaries receive no credit for the trustee's 30% minimum tax:

- The trust pays 30% minimum tax on the distribution to the company.

- The company then pays its own tax when distributing to shareholders — with no offset from the trust's 30%.

- Total tax on the same income can exceed 55% in some scenarios — significantly worse than paying tax as an individual.

- The bucket company strategy is effectively eliminated as a tax-saving tool.

Which Trusts Are Covered — and Which Are Not

- Discretionary trusts (family trusts)

- Most small business trusts where the trustee has discretion over distribution amounts and recipients

- Fixed trusts — beneficiaries have defined, non-discretionary entitlements

- Widely held trusts — managed investment trusts, listed unit trusts

- Complying superannuation funds (including SMSFs)

- Special disability trusts

- Deceased estates

- Charitable trusts

Which Income Is Excluded from the Minimum Tax

- Primary production income — farm and agricultural businesses are exempt

- Certain income for vulnerable minors — protective trust arrangements for children with special needs

- Amounts subject to non-resident withholding tax — income already taxed at source

- Income from discretionary testamentary trusts in existence at Budget night — trusts set up under a will that existed at 12 May 2026 retain their existing tax treatment for this income

Franked Dividends — An Additional Rule

If a discretionary trust receives franked dividends, the trustee must use those franking credits to offset the 30% minimum tax before using cash. This prevents trusts from preserving franking credits while paying the minimum tax in cash.

Trading Trusts vs Passive Investment Trusts

If the business principals are already earning above ~$45,000 and paying 30%+ tax, the minimum tax adds little extra burden — the credit covers the trustee's payment, and they pay the remaining difference at their marginal rate as before. The real loss is the ability to distribute income to lower-rate family members, which the minimum tax specifically eliminates.

Similar impact — investment income can no longer be effectively streamed to low-tax beneficiaries. Combined with the separate CGT changes from 1 July 2027, capital gains flowing through a discretionary trust also face a 30% minimum tax on the gain. Both floors apply simultaneously — the income-splitting flexibility that historically made these structures attractive is significantly eroded.

Restructuring Options — The 3-Year Rollover Window

The Government is providing a 3-year tax-free restructuring window from 1 July 2027 to 30 June 2030. During this period, businesses and investors can move assets out of a discretionary trust into a company, fixed trust or other entity without triggering income tax or CGT. Ordinarily this would be a taxable event, so this rollover is a meaningful opportunity to restructure.

Options to consider (professional advice is essential before acting):

- Transition to a company: If principals are already on 30%+ tax rates, a company at the 25% small business rate may be simpler and equally effective for retaining profits.

- Convert to a fixed trust: If income can be allocated to beneficiaries with defined entitlements, a fixed trust falls outside the new rules.

- Do nothing: If all beneficiaries already pay 30%+ tax, the minimum tax adds no extra net tax — only additional compliance. Restructuring may not be warranted.

- Pay market-rate salaries to working family members: Wages paid for genuine work remain deductible to the trust and are not affected by the minimum tax.

Who is Most Affected?

- Families distributing trust income to adult children, stay-at-home spouses or low-income beneficiaries

- Business owners running operations through a trust with a mix of high and low-rate beneficiaries

- Investors using bucket companies to park and defer trust income

- Passive investment trusts with low-rate beneficiaries

- Trusts where all beneficiaries already pay 30%+ tax — no extra net tax

- Farm trusts — primary production income excluded

- Fixed trusts, super funds, deceased estates, charitable trusts — excluded entirely

- Trusts distributing to income support recipients — exempt from minimum tax

Teachers often pay for their work-related expenses out of pocket. If you are a teacher, you can claim the following. You can only claim a deduction if 1) you spent the money and were not reimbursed, 2) was directly related to your income and 3) have a record to prove it.

Teachers often pay for their work-related expenses out of pocket. If you are a teacher, you can claim the following. You can only claim a deduction if 1) you spent the money and were not reimbursed, 2) was directly related to your income and 3) have a record to prove it. If you are a factory or warehouse worker, you can claim the following deductions. You can only claim a deduction if 1) you spent the money and were not reimbursed, 2) was directly related to your income and 3) have a record to prove it.

If you are a factory or warehouse worker, you can claim the following deductions. You can only claim a deduction if 1) you spent the money and were not reimbursed, 2) was directly related to your income and 3) have a record to prove it.